Your credit score is one of the most important aspects of your financial health. A high score opens the door to better loans, lower interest rates, and greater financial freedom. But many people unknowingly make mistakes that can lower their score, leading to higher debt and more stress.

Let’s dive into the 12 credit score blunders that are likely damaging your financial future and show you how to fix them before it’s too late.

Maxing Out Your Credit Cards

Maxing out your credit cards is like playing a dangerous game of financial roulette. It feels harmless at first, but it’s a surefire way to ruin your credit score. A high credit utilization rate, which is the percentage of your total available credit that you are currently using, signals risk to lenders and hurts your score. Even if you can afford it, maxing out your credit is a big mistake.

Fix It: Aim to keep your credit utilization under 30%. If you’re nearing your limit, pay it off as soon as possible. The less you owe in relation to your available credit, the better your score will look.

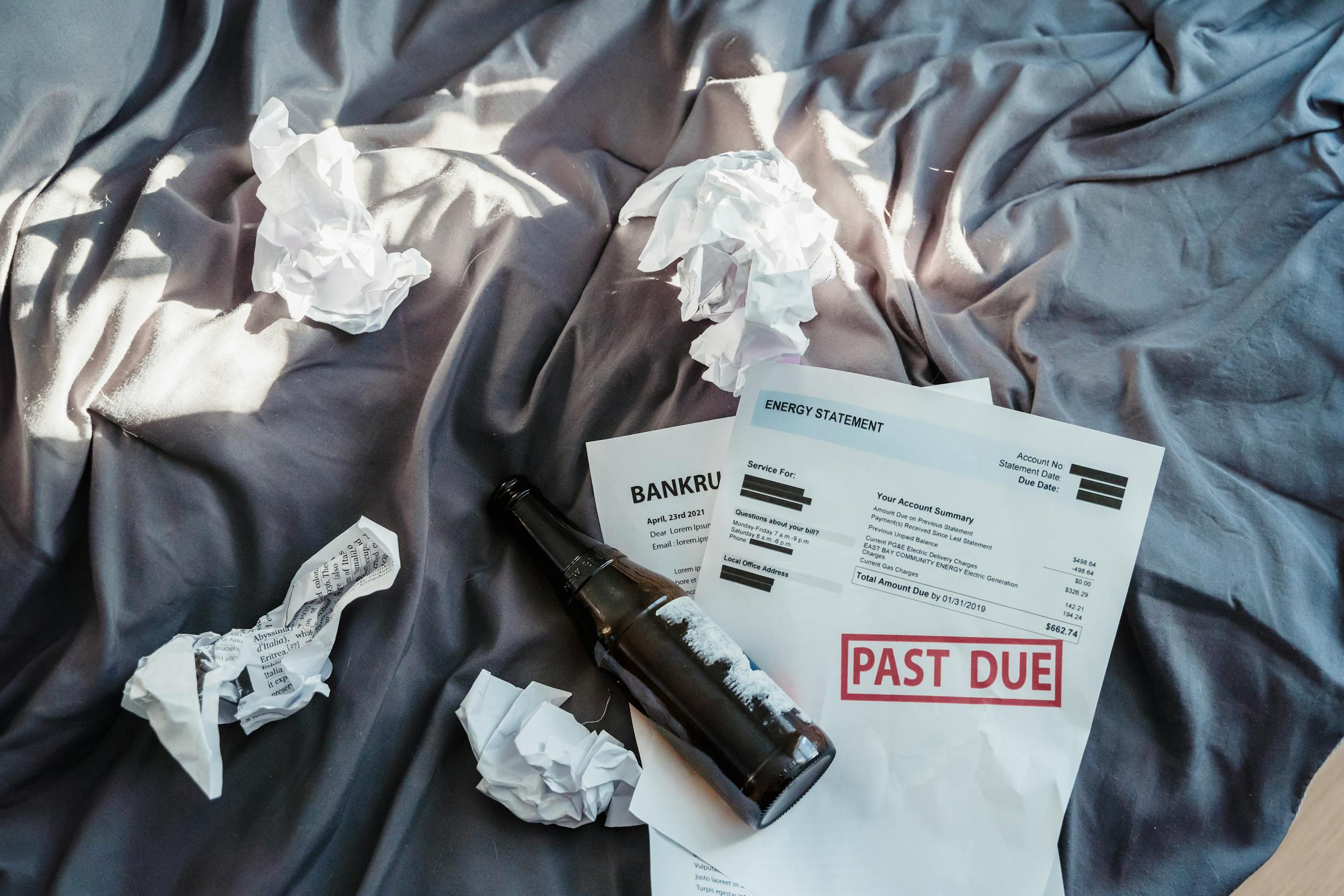

Letting Bills Go Unpaid

You might think that missing a bill or two won’t hurt your credit, but unpaid bills can quickly show up on your report and drag down your score. Whether it’s a utility bill, medical expense, or missed rent payment, if it goes to collections, it could stay on your credit report for years.

Fix It: Pay your bills on time or set up automatic payments to avoid missing deadlines. If you can’t pay, call your creditors to work out a payment plan before it’s too late.

Closing Old Accounts

You might think closing an old credit card you rarely use is a good idea. However, shutting down old accounts hurts your credit score in two ways. First, it reduces your available credit, raising your credit utilization ratio. Second, it shortens your credit history, which is a key factor in your credit score calculation.

Fix It: Keep old credit accounts open, especially if they have no annual fee. The longer your credit history, the better your score.

Missing Payments

Missing a payment, even just once, can have a dramatic effect on your credit score. Late payments are one of the most significant factors in credit scoring models and can stay on your credit report for up to seven years. That single missed payment can haunt you, making it harder to qualify for loans or get favorable interest rates.

Fix It: Set up automatic payments or reminders to ensure you never miss a due date. Even paying the minimum on time is better than missing a payment altogether.

Co-Signing Loans

When you co-sign a loan, you’re essentially taking on someone else’s debt. If the primary borrower defaults or misses payments, your credit score takes a hit, too. Even if you trust them, this is a financial risk that can backfire quickly.

Fix It: Only co-sign for someone you trust completely, and even then, understand the full risk you’re taking on. If possible, avoid co-signing altogether.

Applying for Too Much Credit

It’s tempting to apply for multiple credit cards or loans when you’re trying to build credit or make a big purchase. However, each credit inquiry can lower your score. Too many inquiries in a short period can signal that you might be struggling financially.

Fix It: Be selective about when and where you apply for credit. Space out your credit applications and only apply when absolutely necessary.

Ignoring Your Credit Report

You can’t improve what you don’t monitor. If you haven’t checked your credit report recently, you might be missing errors that are damaging your score. These errors could range from outdated personal information to incorrect debts or accounts, and they can stay on your record for years. Your credit report is a detailed summary of your credit history, so it’s important to review it regularly.

Fix It: Check your credit report regularly (at least once a year) and dispute any inaccuracies. It’s a quick fix that could have a major positive impact on your credit.

Not Using Your Credit

It might sound counterintuitive, but not using credit can hurt your score. Lenders want to see how you handle debt. If you have a credit card you never use, you’re essentially invisible in the eyes of credit bureaus, and that can hurt your credit score.

Fix It: Use your credit cards for small purchases and pay them off in full each month. This shows lenders that you’re responsible and capable of managing debt.

Declining Credit Limit Increases

When your credit card company offers to increase your credit limit, many people decline the offer because they’re worried about overspending. But refusing an increase could hurt your credit score by raising your credit utilization ratio. More available credit means less risk.

Fix It: Accept credit limit increases. More available credit lowers your utilization ratio, which boosts your score.

Bankruptcy or Foreclosure

Bankruptcy or foreclosure can feel like the only option when financial trouble strikes, but these are among the most severe blows to your credit score. These events can stay on your credit report for up to ten years, making it incredibly difficult to rebuild your credit and secure loans.

Fix It: Avoid these extremes by working with a financial advisor or credit counselor. Look into debt consolidation or negotiating with creditors before resorting to bankruptcy or foreclosure.

Adding Someone with Poor Credit Habits as an Authorized User

You might think adding a friend or family member as an authorized user on your credit card is a harmless way to help them build credit. But if they miss payments or rack up debt, their poor habits affect your score too.

Fix It: Only add someone as an authorized user if you trust their financial responsibility. Don’t let someone else’s mistakes ruin your credit.

Relying on Credit Alone to Build Your Score

A credit card or loan might seem like the easiest way to build your score, but it’s not the only way. Many people rely solely on credit cards to build their credit, forgetting other ways to demonstrate their financial responsibility.

Fix It: Consider taking out a small personal loan or adding a mix of credit types (like installment loans) to your credit portfolio. This can boost your credit score by showing you can handle different types of debt responsibly.

Conclusion

Your credit score doesn’t just reflect your ability to manage debt; it’s an essential part of your financial future. Avoiding these 12 credit score mistakes is the first step toward better financial health and more opportunities. The road to a better credit score may take time, but the changes you make today will have a lasting impact on your financial future.

What changes will you make to protect and improve your credit? The sooner you act, the sooner you’ll reap the benefits. Let us know in the comments how you’re taking control of your credit score!